Making Insurance easy to understand so you can make good choices all the time

Life is full of risks and unexpected things can happen at any time and they can have a devastating effect on your life, your family, what you own or your ability to earn a living. That is why we have insurance, its one way that you can reduce the financial and emotional impact should the worst happen.

But the world of insurance is complex. Customers are buying an intangible product that can often be confusing and complicated with technical terminology, conditions, obligations, jargon and product documents with many pages outlining what you are or are not covered for.

At the same time, insurance is an important part of your financial resilience and wellbeing - if you understand insurance, then you're able to make more informed choices about your finances and risk management practices.

So, we have developed this guide to help breakdown the confusion, jargon and complexity of the world of Insurance and help answer questions you may have. Our aim is to make insurance easy to understand, making it easier to make the right decisions when it comes to protecting what’s important.

1. So What is Insurance?

Insurance is a contract, represented by a policy, in which an individual or entity receives financial protection or reimbursement against losses from an insurance company.

The Insurance company does this by charging their clients a premium to create a big pool of money so that anyone who is unfortunate enough to suffer a loss is reimbursed from the pool. This makes payments more affordable for the insured.

But we must remember insurance is a business and not a service that helps people in times of need. Insurance companies operate to make a profit therefore for Insurance to work they need to collect more in premiums than they pay out in claims and administration.

On the flip side, if you have no insurance and an accident happens, you may be responsible for all related costs. Having the right insurance for the risks you may face can make a big difference in your life. So, it’s a question of risk…

… And as an individual we react to risk in 4 ways:

For example, you've bought a car and you want to protect it from damage, you can:

|

01. Avoid If you avoid the risk, it means either not buying a car or not driving it anywhere |

02. Accept If you accept the risk, you know you might crash it you may or may have not save the money to buy a new one or repair it. |

|

03. Reduce If you reduce the risk, you regularly pay to get a service, change tyres and don't drive in busy traffic |

04. Transfer it If you transfer the risk, you pay an insurance company to insure your car, knowing that if you crash it accidentally then the insurance company will pay to repair or replace it for you (less your policy's excess. |

You can do any combination of these things to manage the risk of damage to your care and each one has different costs and benefits, but the last point is why we have an insurance industry.

Therefore insurance companies manage and transfer your risk by providing protection against a predictable event that may arise unexpectedly in return for the payment of a premium.

That said, we all have the option to self-insure and personally find the money needed in the event of loss or they can buy insurance by taking out an Insurance Policy. If you can, try and build your own pool of money to minimise the cost of insurance.

2. How does Insurance work?

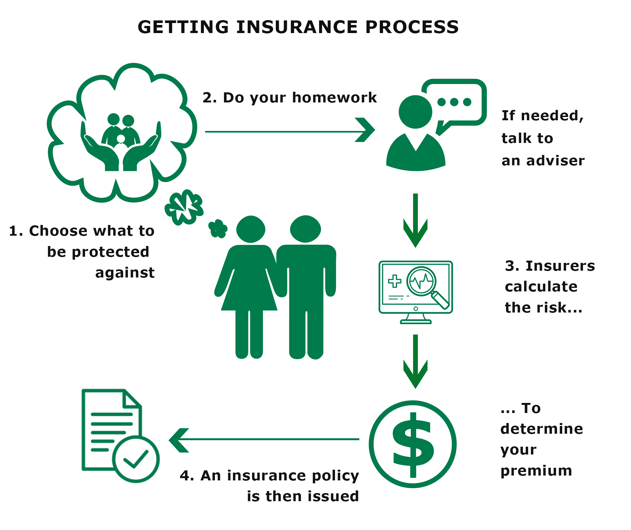

With insurance, you choose what you want to be protected against.

Then, you do your homework as not all insurance policies are the same. Better still talk to an adviser who can help you work through your options before you choose your Insurer.

Then your chosen insurer calculates the risk and probability that the events to be insured will happen and the insurance provider or insurer will determine the price you will need to pay (your premium or subscription).

An insurance policy is then issued and that’s a legal contract between the policyholder (the person or company that gets the policy) and the insurer (the insurance provider), in which the person or company receives financial protection or reimbursement against losses from the insurance company.

Insurance policies are often in place for a specific period of time. This can be referred to as the policy term. There are a multitude of different types of insurance policies available, price and terms will be based on the insurers perception of the risk. But the core components of an insurance policy don’t really change. They are the premium/subscriptions, the policy cover, terms and conditions and the Excess if any. To select the best policy for your circumstances or needs, it is important to understand them:

- The Premium: A policy's premium is its price, sometimes expressed as an annual cost but usually the premiums can be paid at more frequent intervals. The premium is determined by the insurer based on how much of a risk the policyholder is to the insurer. The higher the risk the higher the premium.

- The Policy Limit: The policy limit is the maximum amount an insurer will pay under a policy for an insured loss. Maximums may be set per period (e.g., annual or policy term), per loss or injury, or over the life of the policy, also known as the lifetime maximum. Typically, higher maximums carry higher premiums .

- The Excess: This is a specific amount the policy-holder must pay out-of-pocket before the insurer pays a claim. Policies with very high excesses are typically less expensive because the high out-of-pocket expense generally results in fewer small claims.

- Terms and Conditions: These are specific provisions, rules of conduct, duties, and obligations that the insured must comply with in order for coverage to begin or must remain in compliance with in order to keep coverage in effect. If policy conditions are not met, the insurer can deny the claim.

- Duty of Disclosure: When you apply for insurance you have a legal duty of disclosure. This means the insurer will rely on the information it receives to decide on the terms and conditions for your insurance. The insurer will ask for certain particulars and you must provide all information that an insurer might need to know, including information from your past as well as up to date and relevant information in response to any questions asked.

You must also tell the insurer of any information that you may have that will be material to the risk you wish to insure. This includes any information that could influence the decision of a prudent insurer to decide whether to accept the insurance and if so, the terms that will apply including the level of premium, limitations on cover, excess or any other special requirements. If in doubt, you should give information to the insurer for consideration.

The disclosure duty exists not only when the insurance is taken out but with some types of insurance (typically on your house, car and boat insurances),it also applies at each renewal of the policy and during the currency of the policy. Non-disclosure may either be innocent (an oversight) or fraudulent. Unfortunately, it is usually only detected at the time of a claim and may lead to the claim being rejected can also lead to policy being cancelled.

3. What Insurance I need?

To find out how much insurance you need, ask yourself these five questions:

- What is the risk or event that I would be insuring against?

- What are the chances of it occurring?

- What would happen?

- How much would it cost?

- Who would be impacted?

Once you have established the answers you can then work out what insurances are most important to you when you’d be badly affected by a loss – even one that is not very likely to happen.

Remember, the types of insurance that you need will depend on what you need to protect and what’s important to you. For example: If you have children, what would happen to them if you died unexpectedly? A life insurance pay-out could help make sure they’re looked after financially. Or if you have a mortgage, what would happen if you became too ill to work? Income or Mortgage Protection Insurance could help cover your payments and living costs.

4. Common Types of Insurance

Here are some common types:

4.1 Insure what we own- Home Insurance: Most home insurance provides cover only up to the ‘sum insured’ – a capped amount that is the limit of what we can claim . You need to decide what your sum insured is – how much it would take to rebuild your home in the event of a disaster. You also need to include the cost to clear the property prior to a rebuild. House insurance is usually required by a lender when we have a mortgage. Lenders mortgage insurance covers the bank if we can’t make the payments on our loan.

- Contents Insurance covers damage and loss of our belongings. It also provides some ‘third party’ cover if we damage someone else’s belongings in the house we are living in or if you damage your neighbour’s property. It’s also a good idea when flatting or renting to insure your valuable possessions including any computers and musical instruments.

- Insuring our Car: Next to houses, cars can be one of the most expensive items we will own. If your car is damaged in an accident or stolen it can be very expensive to repair or replace. By taking out an insurance policy you transfer that risk to the insurer who will pay to repair or replace your car if these events occur. However, if you cause an accident whilst breaking the law e.g. driving under the influence of liquor, drugs or driving too fast you are unlikely to be covered.

The cost of insurance will vary depending on our age, claims history, location including where the car is parked at night, the level of excess we are prepared to take, and the make and type of vehicle.

Comprehensive’ motor vehicle insurance

The most common and it covers us for loss, theft or damage to our vehicle. It also covers us for accidental damage to the other car or property we damage.

Third Party and Third Party, Fire and Theft’ cover.

Third party insurance covers for damage to another person’s vehicle or property, but not yours. Extending third party insurance to fire and theft covers the risk of our car being destroyed by fire or stolen, too.

There are many types of health-related policies, such as:

- Medical Insurance which covers medically necessary private hospital treatment and can include other day to day medical bills

- Trauma (also called critical illness) which provides a lump sum if you suffer from certain named illnesses or injuries such as cancer, heart disease or paralysis

- Income Protection Insurance which pays a percentage of your income on an ongoing basis if you suffer illness or injuries and are unable to work for an extended period

- Mortgage Protection Insurance which covers your mortgage repayments if you can’t work due to illness or accident

- Disability Insurance which pays out a lump sum for total and permanent disablement if you are so disabled that you can never work again

4.3 Insure our Lives

There are different types of life insurance cover. The most common one today is term life insurance, which provides cover for a fixed number of years usually until age 99 (or until you no longer require it). Or there is funeral insurance. Note, with both life and funeral insurance if you cancel your plan prior to an event that could result in a claim, you will not receive any refund of your premiums paid.

- Life Insurance provides a lump sum of money on death to a named person. The money from your life insurance policy can help your family, repay debt, pay bills (including funeral costs) and cover living expenses.

In most cases the ‘sum insured’ will be paid out early on the diagnosis of a terminal illness. With life insurance it is important that you carefully select the person (beneficiary) who will receive the payment in the event of a claim.

It is important to review your needs, including the policy ownership every few years as otherwise at claim time the payment of any benefit might be paid to someone you no longer would want to receive it (such as an ex- spouse). Most life insurance policies also do not cover death by suicide for the first 12 or 13 months. - Funeral Insurance or Funeral Cover as it’s more commonly known is a financial helping hand you can provide for your family. When you pass away, your family will receive a lump sum benefit payout they can use to cover any immediate expenses, such as a funeral service or outstanding debts. With funeral cover, for the first 2 or 3 years a payment will only be made if the cause of death is an accident. Thereafter a payment will be made irrespective as to the cause of death.

4.3 Insuring our Travels

It’s a good idea to buy travel insurance for any holiday where a cancellation of your plans will result in significant financial loss. Medical bills can be very high in other countries, and it’s a big financial risk to go on holiday without travel insurance.

Travel insurance policies cover belongings against loss or theft, extra costs if flights are cancelled, and medical treatment if you have an accident or become ill and repatriation home in the event of an accident or death.

5. What to consider when buying insurance

Buying insurance is a big decision and can have huge implications on the quality of your life. That's why you should approach the decision in an informed and calculated manner.

Most people really only think about their insurance when a loss, injury or accident has occurred. This is the time you need financial assistance the most and your insurance company needs to come through for you, help you get treatment or provide a payout to get you back on track in life. After all, this is what you pay them for.

However for that to happen you really need to have put in the hard yards in first to make sure your policy is covering you the way you thought it was.

Insurance is complex and not all insurance policies are the same. It’s easy to compare two policies on price, but the cover you get may be very different. The cheapest policy isn’t usually the best cover for your needs, and it’s important to compare both the price and the level of cover.

So when buying insurance, you should always do your homework or better still, get an expert to do it with you.

Be careful as the policy that is cheaper today may not be the best structure for you long term. For example with Life Insurance, your choice may come down to whether your need it on a shorter timescale - like covering a mortgage or permanent - leaving an inheritance for someone.

A crucial point to remember is that your insurance policy is a legal contract and is legally binding to both the insurer and the insured (the person taking out the insurance). In the event of a claim it is the wording of the insurance policy (the contract) that will determine the eligibility, or otherwise, of your claim. It is up to the insured to make themselves aware of what obligations they have under the policy and also what obligations the insurer has.

6. Get the right advice

Do you know that comparison sites are not always the best way to compare insurance policies?

Some of the policies you’ll be offered can be fairly generic so if you want a policy that meets your individual circumstances it might be better to use a specialist.

A qualified Financial Adviser can help work out exactly what you need cover for and customise insurance cover specifically for you.

They can be invaluable in sourcing the best deal for you, customised to suit you perfectly. And, in the event you need to make a claim, an adviser can help you through the claims process – removing the stress so you can focus on you and your loved ones.

Here are a few reasons why going to a Financial Adviser for insurance might be the best choice:

Getting expert guidance does not cost you more

Like comparison sites they get paid commission by the insurance provider for selling their products so you don’t pay them a fee for shopping around to get you the most appropriate plans for your needs

Unlike comparison sites they have specialist expertise and can give you guidance on the products that best suit your needs.

They know all the options

Insurers won’t always offer you every type of cover when you go directly to them. Financial Advisers can help point out the types of cover available for the insurers they represent and help you work out what you need.

They will find you the right product for you

A Financial Adviser will ask you about your personal circumstances to find you the right policy. They’ll also be able to tell you if you’re already covered by your existing insurance policies so you don’t overlap, and they will often get you a good deal by comparing prices and product features

Find Specialised cover

If your need is specialised they can find tailored cover to suit your needs

Continue to Support you

If you need to make a claim, your Financial Adviser can support you by taking away the hassle and worry during a stressful time. Also, if your circumstances change they are on hand to review your cover to make sure it’s still right for you.

At HealthCarePlus, we have access to a nationwide team of Monument Financial Advisers. For over 30 years Monument Insurance has been HealthCarePlus’s appointed business partner to provide financial advice to HealthCarePlus Members on life and health insurance. So if you’d like to talk to one of them from your area, you can book a time for a free no obligation chat about your circumstances and what could be right for you.

7. Buying Insurance Checklist

When buying insurance, having the necessary information gathered beforehand will make the process much easier. So before you commit to it, we suggest running through this checklist below.

7.1. Look at the Insurer and their Credit Rating

Research any insurer you’re thinking about buying from to be sure that the company is financially sound and provides good service.

Look at their credit rating. The higher the rating, the more certain you can be about the company’s ability to pay claims and be around for the long term. An A rating is the best.

7.2. Choose the right excess

When choosing a high excess, the premium will be lower, because the insurer is covering less of the cost.

But the trade-off is that you’ll also have to pay more for each claim. It’s good to choose a policy excess that matches the point at which it would become a struggle to make the payment.

7.3. Be honest

By law you must give all information requested by the insurer, even if you think it is irrelevant it may be something that the insurer considers a material fact. Leaving any important information out could risk future claims being turned down.

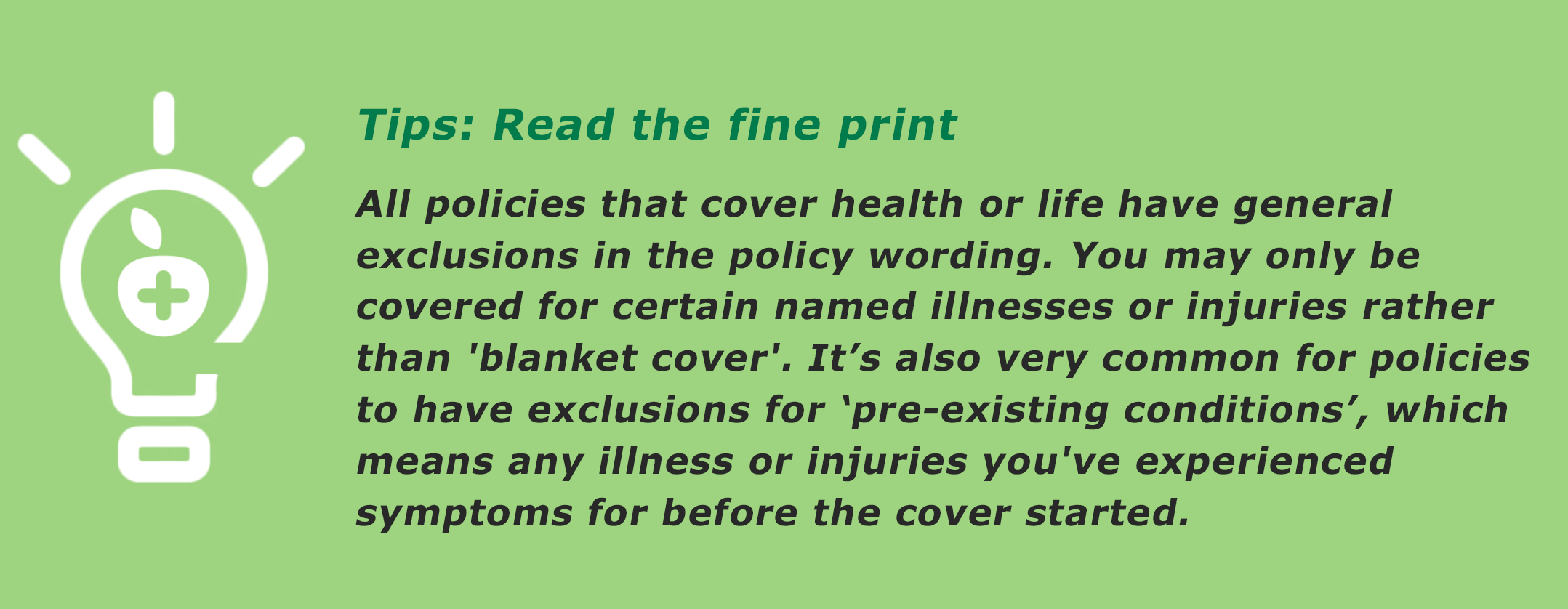

7.4. Read the policy carefully

You need to understand what is, and isn’t, covered by the policy. It’s important to take the time to check it and ask the insurer to explain anything that isn’t clear.

7.5. Don't double up

Some of us already have some types of insurance – for example through work or as part of a loan agreement.

7.6. Shop around

It pays to get a range of quotes and compare, looking closely at what is and isn’t included by each policy.

7.7. Combine insurance

Buying as much insurance as possible from one company can save money, so it’s good to consider the options and see what’s best for you. As always, you need to consider the product and price to gauge if it’s worth it.

7.8. Take precautions

There are things you can do which can reduce the premiums you pay. For example, for your home and car, such as installing an alarm.

7.9. Beware of buying insurance offered alongside something else

For example, you might be offered travel insurance when you book a holiday. If you need this insurance, you might get it cheaper with better cover elsewhere once you’ve looked around

7.10. Have you compared like with like?

Watch out for how different charges, types and levels of cover, and your excesses are calculated when you compare policies.

7.11. Review before you renew

It’s important to check your coverage each year when you renew your insurance, or whenever your circumstances change.

7.12. Read 'Good to know' Insurance Guide

Make sure you read through our 'Good to know' guide about Insurance. You can download it from here.