Making Health Insurance easy to understand so you can make good choices all the time.

Helping to improve our Members financial well-being is a core part of why we exist and along with our commitment to education and knowledge we are developing a series of resources to help our Members become more financially resilient.

This guide outlines some of the reasons you might choose private healthcare and how insurance can help you to access and fund this. Health insurance can help you to take care of your everyday wellbeing, aids a speedy diagnosis and recovery through reduced waiting times, and helps to pay for some or all of the treatment that you need.

1. So What is Health Insurance?

The New Zealand public health system and ACC does a good job in providing access to treatment for serious illness and emergencies.

However, many health issues Kiwis face are either not accidental or are for non-urgent health conditions like hip replacements or cardiac procedures and there are often delays in accessing the treatment and it can cost thousands.

Going without treatment for these conditions can have a huge impact on a person’s quality of life.

With Health Insurance, you can have choices around:

- who you elect is insured in your family

- the types of treatment covered

- the level of cover to apply to those treatments

- the location where your treatment is provided

- the contribution you might be willing to make towards the treatment cost (called ‘the excess’).

2. Why get health insurance?

So, do you need health insurance or don’t you? That’s the million dollar question.

There are two key reasons:

2.1. Increasing Demand and Pressure on The Public Health System

Whilst New Zealand has one of the best public healthcare systems in the world and New Zealanders enjoy comprehensive medical treatments irrespective of their income level, savings or age, the system is under continuous pressure to cope with increasing demand.

Demand for medical treatment will continue to rise faster than the country’s ability to fund it through taxes. To manage this cost, public health systems use a points system to manage access to treatment and you need to have enough “points” to be eligible for treatment.

Our population is growing, ageing, diversifying and life expectancy is increasing faster than health expectancy (the time spent in good health), so more people are spending longer in poor health.

Plus, not all treatments or costs are covered by the public health system, and you often have no control over the timing of the care you need. So, it is common for people to endure a long and uncomfortable wait until a condition worsens enough for them to be treated in the public health system.

This means you will either pay for your own non-urgent healthcare costs or wait longer for treatment in the public health system.

2.2 Future Planning

You don’t know what health problems may affect you in the future and you cannot foresee how they will impact on your family, your lifestyle or your earning ability.

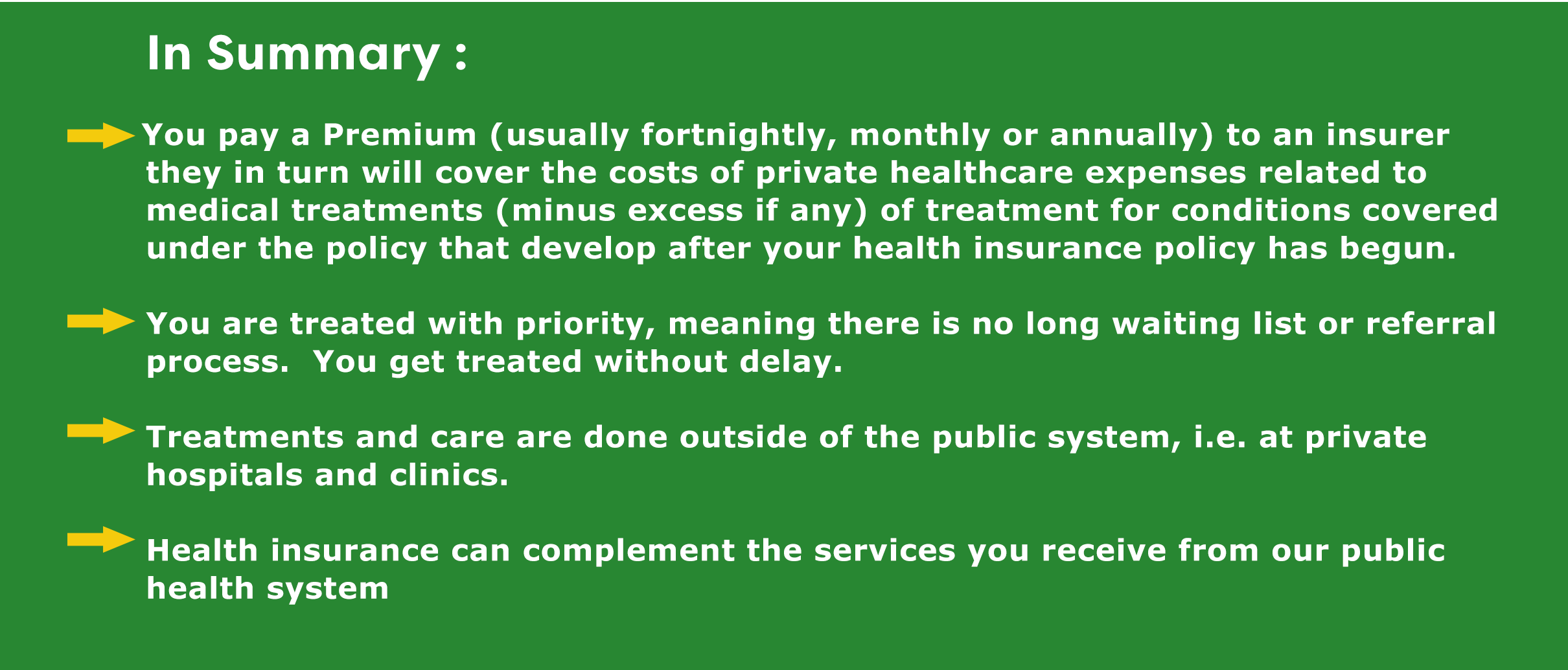

That is why health insurance offers people the peace of mind that treatment can be obtained in a timely manner and that all or most of their future treatment costs will be covered.

So Having health insurance means that you have access to treatment without facing a lengthy wait. You also have the assurance that you can recover all or most of the costs.

|

Health insurance takes away the uncertainty of your future health care Health insurance makes an enormous contribution towards the health and well-being of New Zealanders, funding around half of all elective surgery and over $1 billion in healthcare treatment costs each year. |

3. The different types

Most insurers offer a range of plan levels – from extensive cover through to basic core policies covering surgical treatment only. Often insurers offer plans with add-ons for services such as diagnostic, optical or dental cover.

In addition to the plan type, most insurers will provide a range of excess options, with higher excesses linked to lower premiums. This means you can tailor the level of cover you need to your particular needs or circumstances. That said there are 3 main types of private health insurance available in New Zealand:

| Primary Care | Sometimes called Minor Medical or Day-to-Day Insurance. These products provide cover for day-to-day medical treatments, but provide little or no cover for more significant major surgery or treatment costs. |

| Major Medical | Major medical policies typically provide cover for elective surgery, major treatments, and the cost of specialist visits, but do not cover day-to-day medical expenses. |

| Comprehensive | Comprehensive health insurance products provide cover for both major surgery and day-to-day medical expenses. |

4. Understanding your cover

To make sure that you understand what you are covered for and the limits that will apply if you make a claim, it is really important to read the policy terms and conditions. So here is a quick guide to the 7 key terms you should be looking out for when evaluating your cover.

4.1. The Cost

The price of your health insurance can depend on your age, the excess you’re willing to pay, whether you’re a smoker, your gender, the type of cover you need and your current health status.

For example: Insurance companies look at your age because that can predict the likelihood that you'll need to use the insurance. With health insurance, younger people are less likely to need medical care, so their premiums are generally lower. And remember, health insurance premiums will usually go up annually due to the increases in medical inflation and expected utilisation in line with each member’s age.

4.2. The Excess

An excess is the amount of money you need to pay towards the total cost of any claims you submit. Insurers will offer different excess options that can help to make your premiums more affordable. The higher the excess, the larger the discount on your premium.

4.3. Pre-existing Conditions

Your medical history, or any pre-existing medical conditions may affect what you can get health insurance cover for.

For example, if you've had a heart attack in the past 12 months, your insurer will want the full details of your condition, but it's highly likely that heart related issues won't be covered in the future.

Each insurer has differing approaches when it comes to how they will approach exclusions. It will depend on your pre-existing condition, and what it's associated with it.

3 ways an Insurer will deal with pre-existing conditions:

- Permanently exclude the condition from your cover

- Charge an additional premium to cover the condition

- Only cover the condition after a “stand-down” period. A “stand-down” period means that cover will be available for the condition after your policy has been running for a set time, this is normally around three years.

4.4 Exclusions

Not every kind of medical condition or treatment can be covered, so there are some things that may have to be excluded from your cover. There are usually two types of exclusions:

a General Exclusions: These are general things such as a medical condition or service that a health insurer decides that they we will not cover for anyone who has the same type of policy. These will be listed in the “what is not covered” section of a policy document.

List of common exclusions:

- HIV/AIDS and related medical conditions

- Fertility Treatment

- Cosmetic Treatment

- Treatment in a public hospital or covered by ACC

- Illness caused or contributed by drug or substance abuse

- Gender Reassignment Surgery

- Senile Illness or Dementia

- Any Sexually Transmitted Disease

- Self-inflicted injuries Overseas Treatment except is specifically included in the policy

b. Personal exclusions: These are specific to an individual and will be based on your medical history (pre-existing conditions). These conditions will be listed on your membership certificate for each individual.

4.5. Cancer Cover

Surgical and Medical Cancer Treatment Cancer care is usually included in a Major– or Comprehensive policy, and will typically cover treatments like chemotherapy, radiotherapy, surgery, hormone therapy, psychological counselling and alternative treatments like acupuncture. Some types of Cancer treatment may not be included, or cover may be restricted to a lower maximum level of reimbursement.

4.6. Stand down or waiting period

A stand-down period doesn’t allow you to claim for services within an initial period when you take out cover. These stand-down periods are detailed in your policy document and once your stand-down period has ended, you will usually be informed that you are now able to submit claims for services used and cost incurred after the stand-down period.

4.7. Non-PHARMAC Drugs

In New Zealand, PHARMAC a government agency is responsible for deciding which medications are funded through the public health system and which are not. While PHARMAC covers the cost and or subsidises many medications, there are a handful of treatments, some of them potentially life-saving, which are not covered, usually because these drugs are very new or extremely expensive. For example Cancer drugs can be prohibitively expensive without PHARMAC funding.

So having medical cover that provides an adequate level of “non-PHARMAC” cover can be beneficial – it’s better to have medical insurance in place (with the right policy) than leave things to chance and discover only upon becoming ill that one's best hope of recovery is not funded via the public health system. Due to the cost of “non-PHARMAC” subsidised drugs, the inclusion of this benefit in your policy can be costly.

5. What to consider when buying health insurance

If you've decided, you can afford health insurance there are a few things you need to think about when choosing a provider:

- The reputation of the insurer. Is it trusted and respected? If you have not heard of the insurer ask a financial adviser about the insurer and their reputation.

- Its range of plans. Does it have what you need?

- Its financial stability. Will it be there when you need it?

- Its customer service especially claims service.

- Sustainability of the insurer. Remember if the deal looks too good to be true it probably is.

There is no one best health insurance policy, but the best one for you will depend on the type of health insurance you need and your budget so shop around and remember it’s about YOU and not your neighbours or friend’s experience.

Choosing the right plan and how much cover depends on your stage in life and general state of health. You need to think about whether you want cover for major medical costs, like surgery and hospital treatment, or also want to claim for day-to-day things like visiting your doctor and dentist.

But here are six things to consider when looking around:

- Your Pre-existing conditions and how the health insurer will deal with them

- What can you afford – i.e size of premium vs size of the excess and this is not only today, but what about in 10 years’ time when you may really need the cover?

- The level of Cancer Cover: Surgical and Medical Cancer Treatment

- Non-PHARMAC Drugs covered or not

- Guaranteed benefits and future upgrades

- Are you eligible for any “special deals” via your Union or other organisations that you or your partner is a member of?

These questions will help you to work out what kind of health insurances are most important to you when you’d be badly affected by a loss – even one that is not very likely to happen.

6. How much it cost without health insurance

When unexpected medical events happen, the true cost of surgery can take many Kiwi families by surprise.

Due to the demands placed on our public health system, waiting for treatment that you won’t need to pay for, can take about 10 months - which can impact your ability to work and earn, your recovery, and your family.

For New Zealanders who elect to pay from their own hard-earned savings to get faster, private surgery, the costs - even in NZ - can be considerable. Below are indicative cost ranges, for common types of surgery and common medical tests.

7. Get the right advice

Do you know that comparison sites are not always the best way to compare insurance policies?

Some of the policies you’ll be offered can be fairly generic so if you want a policy that meets your individual circumstances it might be better to use a specialist.

A qualified Financial Adviser can help work out exactly what you need cover for and customise insurance cover specifically for you.

They can be invaluable in sourcing the best deal for you, customised to suit you perfectly. And, in the event you need to make a claim, an adviser can help you through the claims process – removing the stress so you can focus on you and your loved ones.

Here are a few reasons why going to a Financial Adviser for insurance might be the best choice:

Getting expert guidance does not cost you more

Like comparison sites they get paid commission by the insurance provider for selling their products so you don’t pay them a fee for shopping around to get you the most appropriate plans for your needs

Unlike comparison sites they have specialist expertise and can give you guidance on the products that best suit your needs.

They know all the options

Insurers won’t always offer you every type of cover when you go directly to them. Financial Advisers can help point out the types of cover available for the insurers they represent and help you work out what you need.

They will find you the right product for you

A Financial Adviser will ask you about your personal circumstances to find you the right policy. They’ll also be able to tell you if you’re already covered by your existing insurance policies so you don’t overlap, and they will often get you a good deal by comparing prices and product features

Find Specialised cover

If your need is specialised they can find tailored cover to suit your needs

Continue to Support you

If you need to make a claim, your Financial Adviser can support you by taking away the hassle and worry during a stressful time. Also, if your circumstances change they are on hand to review your cover to make sure it’s still right for you.

At HealthCarePlus, we have access to a nationwide team of Monument Financial Advisers, so if you’d like to talk to one of them from your area, you can book a time for a free no obligation chat about your circumstances and what could be right for you.

![]()

*For over 30 years Monument Insurance has been HealthCarePlus’s appointed business partner to provide financial advice to HealthCarePlus Members on life and health insurance. (HealthCarePlus is not legally able to provide financial advice).